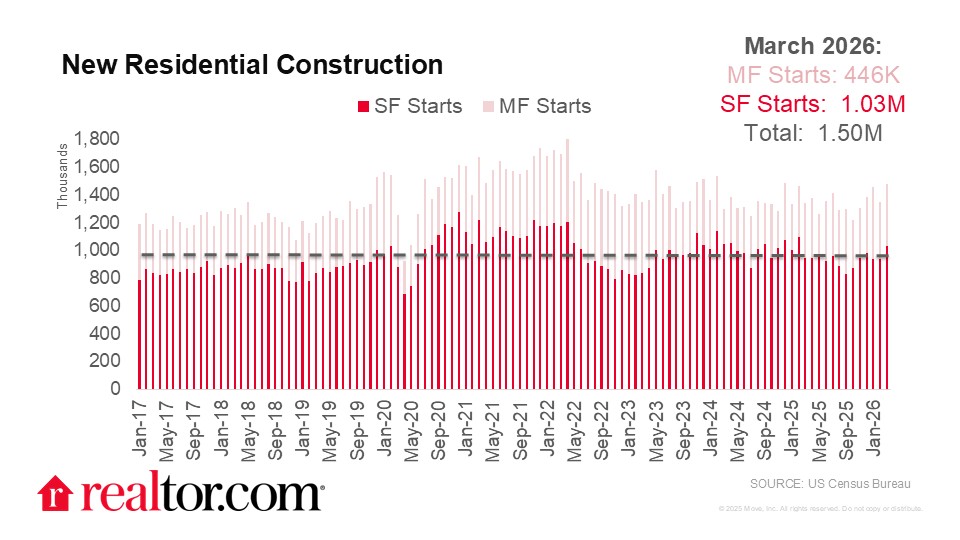

What happened

New residential construction had a strong March in terms of projects started, up 10.8% both month over month and year over year. Permitting and completions were weaker, though. The number of units permitted for construction in March was down 10.8% from a strong February and down 7.4% from March 2025, while the number of units completed was up 0.1% month over month and down 12.8% year over year. The strong starts figure suggests that builders are anticipating stronger buyer demand than what has been seen recently and are willing to work the projects in their pipeline, but the pullback in permitting shows that this optimism is balanced with some caution about the economic realities they face. Builder margins are being squeezed by rising material costs that stem from today’s geopolitical uncertainty on top of the already-high costs of land and labor, so it’s unsurprising to see them exercising some caution about future projects.

Where it happened

The permitting slowdown was concentrated in the South (down 14.0% year over year), which is the region where the most new construction activity currently takes place. Prices are softening in many Southern markets as the inventory of homes for sale exceeds pre-pandemic levels, so builders are responding by pulling back activity in this region. Permits grew the most in the Midwest (up 2.4% year over year), where the opposite is true: markets are still tight and the premium on new construction is high. The inventory recovery has been uneven from region to region, so it is encouraging to see builders concentrating their efforts where they are needed most.

The uptick in starts was focused in another region where housing inventory remains scarce, the Northeast (up 18.9% year over year). The pace of housing starts picked up in both the single-family and multifamily space, which rose 8.9% and 13.5% respectively year over year. The single-family starts pace surpassed 1 million homes for the first time in over a year. The most striking slowdown in the starts data came from the Midwestern multifamily segment, which is not explicitly called out in the data, but overall starts for the region fell by 0.9% year over year at the same time that single family starts rose by 17.8%.

Completed homes fell in every region except the Northeast, which saw a whopping 75.9% increase. Take this data with a grain of salt, as the seasonal adjustments during off-peak months can exaggerate the results, but the non-seasonally adjusted figure is an outlier as well. New homes being delivered in the Northeast is a welcome development for a market that badly needs supply and a lucrative opportunity for builders to take advantage of high market prices on newly built homes there.

What does this mean for homebuyers, sellers, homeowners, and the housing market

Though the strong starts figure makes for an encouraging headline, there is more to the story of new construction this month. Builders are being strategic, waiting to see how the Iran conflict plays out before requesting new permits and delivering finished homes in regions where their margins are currently higher. For buyers it remains a good time to purchase new construction, as price reductions and incentives continue to be offered and some markets have a wealth of new home options to choose from.

{kind=link}